PRB 01-10E

A CLOSER LOOK AT THE

FLAT TAX

Prepared by:

Marc-André Pigeon

Economics Division

23 August 2001

TABLE OF CONTENTS

INTRODUCTION

TAX THEORY

A BRIEF HISTORICAL OVERVIEW

THE FLAT TAX IN OTHER COUNTRIES

KEY FEATURES OF THE CURRENT TAX SYSTEM

ARGUMENTS FOR AND AGAINST

THE BUDGETARY CONSEQUENCES OF A FLAT

TAX

CONCLUSION

REFERENCES

A CLOSER LOOK AT THE FLAT TAX

INTRODUCTION

The ultimate in flat tax reforms would

create a single and simple system comprised of two basic ingredients:

a single

marginal tax rate that would apply to businesses and individuals alike, effectively

replacing the entire tax code, including all of its deductions and credits; and

a large

basic exemption so that the flat tax is not unfair to low-income families and individuals.

Flat tax advocates argue that these

changes would not only lead to a simpler tax system, but also improve economic efficiency,

which means there would be fewer impediments to businesses making decisions for purely

economic reasons and individuals making decisions based purely on their preferences.

Most real-life flat tax proposals fall short of these goals, imposing a uniform marginal

tax rate while retaining many – and, in some cases, all – of the deductions,

credits and tax breaks in the existing system. Hybrid flat tax proposals have been

surfacing and resurfacing in the United States since at least the early 1980s. In

this country, the Canadian Alliance has done much to bring the issue to the fore, recently

proposing its own flat tax but subsequently shelving the idea – at least temporarily.(1) Nevertheless, if the United States is any

guide, the issue is likely to re-appear in the policy arena, especially given the

ever-changing and increasingly complex nature of the taxation system and the strong forces

promoting international harmonization of taxes and regulations.

This paper has three objectives:

To provide

some much-lacking historical and international perspective on the issue. Just how

old is the flat tax idea? Where did it come from? And has it been tried before and where?

To look at

the theoretical and practical arguments for and against a flat tax. Why do some

people support a flat tax while others oppose it?

To determine

the cost of a realistic flat tax plan in Canada, given reasonable assumptions.

TAX THEORY

Before answering these questions, it is

useful to briefly review two key concepts of tax equity from the theory of public finance.

Horizontal

equity means that equal persons should be treated equally in the tax code.

Although no two people are ever perfectly equal, the term usually applies to two people or

families with roughly the same income and social circumstances.

Vertical

equity, the flip-side of horizontal equity, means that people should be taxed

differently based on their ability to pay. For example, a family earning $60,000

with no children is able to pay more in taxes than a family earning $60,000 with four

children, assuming all else is equal.(2)

Other terms – including progressive,

proportional and regressive tax regimes – need to be defined because they turn up

frequently in popular discussions and can easily be abused or confused. Most economists

define a progressive tax regime as one where those with lower income pay a smaller

share of their total income in taxes than those with higher income. A regressive

taxation regime is just the opposite: lower-income persons or families pay a

greater share of their income in taxes than do higher-income persons or families. A proportional

tax regime is one where the same marginal tax rate applies to all persons, regardless

of income, so that everyone pays the same proportion of their income in taxes.

In the extreme, a regressive tax would

mean that low-income earners would pay a higher tax rate than high-income earners.

Regressive taxes, however, are often a lot more commonplace than is generally thought to

be the case. Taxes on food, for example, are “the same” for everyone and

yet are considered regressive because food purchases account for a bigger portion of total

income for a typical low-income individual or family than they do for their high-income

counterparts. The following table helps to illustrate the differences between each

type of tax.

Table 1: Comparing Different Tax

Régimes

|

Progressive

(on all income) |

Proportional

(on all income) |

Regressive

(sales tax on food) |

| Family A –

Upper Income |

|

|

|

| Income |

$150,000 |

$150,000 |

$150,000 |

| Amount subject to

taxes |

$150,000 |

$150,000 |

$10,000 |

| Rate at which income

is taxed |

26% |

17% |

6% |

| Tax paid |

$39,000 |

$25,500 |

$600 |

| Percentage of income |

26% |

17% |

0.4% |

| After-tax income |

$111,000 |

$124,500 |

$149,400 |

|

|

|

|

| Family B –

Lower Income |

|

|

|

| Income |

$40,000 |

$40,000 |

$40,000 |

| Amount subject to

taxes |

$40,000 |

$40,000 |

$10,000 |

| Rate at which income

is taxed |

22% |

17% |

6% |

| Tax paid |

$8,800 |

$6,800 |

$600 |

| Percentage of income |

22% |

17% |

1.5% |

| After-tax income |

$31,200 |

$33,200 |

$39,400 |

In the popular debate, there is also much

confusion about whether a flat tax, which is proportional in a strict definitional sense,

can be effectively progressive, i.e., can it assure that a low-income family or

individual pays less of its total income in taxes than does a high-income family or

individual? Given a sufficiently large basic tax exemption, the answer is an unambiguous

yes.(3) To see why, consider the table below,

where we assume two families (the Smiths and Simpsons, each with a sole breadwinner) and

compare a progressive tax regime with a proportional tax regime.

Table 2: Comparing Progressivity

|

A two-rate progressive tax

regime |

A flat tax with

large exemptions |

A flat tax with

no exemptions |

| The Smith Family – Upper

Income |

|

|

|

| Income |

$150,000 |

$150,000 |

$150,000 |

| Exempted income |

$10,000 |

$20,000 |

$0 |

| Taxable income |

$140,000 |

$130,000 |

$150,000 |

| Marginal tax rate(s) |

17% and 25% |

17% |

17% |

| Tax paid |

$27,000 |

$22,100 |

$25,500 |

| Effective marginal tax rate |

18.0% |

14.7% |

17.0% |

| Tax saving relative to a

progressive regime |

n/a |

$4,900 |

$1,500 |

|

|

|

|

| The Simpson Family – Lower

Income |

|

|

|

| Income |

$40,000 |

$40,000 |

$40,000 |

| Exempted income |

$10,000 |

$20,000 |

$0 |

| Taxable income |

$30,000 |

$20,000 |

$40,000 |

| Marginal tax rate |

17% |

17% |

17% |

| Tax paid |

$5,100 |

$3,400 |

$6,800 |

| Effective marginal tax rate |

12.8% |

8.5% |

17.0% |

| Tax saving relative to a

progressive regime |

n/a |

$1,700 |

-$1,700 |

The first column shows a hypothetical

graduated or progressive tax system (with a $10,000 basic exemption) that imposes a

marginal tax rate of 17% on the first $100,000 of income and 25% for income above that

threshold. Because the Smith family’s income exceeds $100,000, the Smiths pay

both tax rates for a total tax bill of $27,000, or 18% of its income. The Simpsons,

on the other hand, pay only $5,100 or 12.8% of their income. This system is

progressive on two counts. First, in the “formally progressive” sense defined by

William Vickrey, namely because it imposes different marginal tax rates for different

income levels (17% and 25%) and second, because the average tax rate (calculated after

factoring in basic exemptions) is lower for low-income families. The fact that the

Smiths pay more in dollar terms than the Simpsons says little about whether the system is

truly progressive, at least given the way most economists have defined the term. The

Smiths would pay more than the Simpsons even under an extremely regressive (and

improbable) tax system that imposed a 4% tax rate on all the income of high-income

families, but a 17% tax rate on all the income of low-income families. In this

extreme case, the Smiths would pay $5,600 versus $5,100 paid by the Simpsons.

Now suppose there’s a sudden switch

to a flat tax system. The second column shows how a flat or proportional tax –

given a large enough basic exemption (for illustrative purposes, the exemption has been

increased to $20,000 from $10,000 in the progressive regime) – can be at least as

progressive as, if not more progressive than, a “formally” progressive tax.(4) Under this scheme, the Smith family’s

effective tax rate falls to 14.7% and it saves a net $4,900 relative to the progressive

regime, while the Simpson family’s effective tax rate falls to 8.5% and it saves a

net $1,700 relative to the progressive tax system. Again, it must be stressed

that just because the Smiths save more than the Simpsons under this flat tax proposal does

not mean the system is regressive. The Smiths still pay a greater portion of their

total income in taxes than do the Simpsons. It would be hard to avoid this outcome

(i.e., a greater absolute tax saving for the high-income family) given any meaningful

reduction in marginal tax rates. Generally speaking, the most effective way to give

more to lower-income families without an even bigger saving for the wealthy is to have

targeted deductions and exemptions.

Finally, column three shows what could be

called a “doubly” pure flat tax because it has no basic deduction. Under

this system, the Simpsons are unambiguously worse off than under the progressive system or

the proportional system with large exemptions. Meanwhile, the Smiths still fare

better than they do under the progressive system but not quite as well as under the flat

tax with a large basic deduction. This analysis illustrates two key points:

First, a flat tax can be made

effectively progressive with large basic exemptions or some combination of exemptions and

deductions.

Second, people concerned with getting

more dollars to low-income persons relative to high-income persons in absolute terms

should focus their attention on targeted (rather than universal, which is implied in

marginal tax reductions) tax breaks such as tax credits and/or welfare transfers.

A BRIEF HISTORICAL OVERVIEW

The term “flat tax,” at least

insofar as it has gained widespread currency, has been around since 1981, when the idea

was put into the policy arena by Robert Hall and Alvin Rabushka. These two Stanford

academics published a book entitled The Flat Tax containing the essential features

of their proposal which can be summed up in five points.

First, reduce corporate and personal

taxes to 19%.

Second, replace targeted depreciation

schedules with a single, first-year, write-off provision so that firms are taxed on their

cash flow.

Third, eliminate all extraneous business

and personal tax deductions and tax credits that get in the way of establishing a true

“consumption-based” tax, i.e., people are taxed only on what they spend or take

out of the economy. For firms, this means taxes would be calculated on net profits

or, in other words, total revenue minus total costs (inputs, wages/salaries and new

equipment). For individuals, this means taxes would be calculated on total wage,

salary and pension income less a basic exemption (see below).

Fourth, eliminate double taxation of

dividends (already partially accomplished in Canada) and capital gains. Individuals

would no longer pay any tax whatsoever on dividend income or capital gains. The

rationale is straightforward: because dividends are paid out of net after-tax

profits, there is no reason to tax them again in the hands of shareholders. The

rationale for exempting capital gains (at the individual level) is similar, and this is

discussed more fully later in the paper.

Fifth, create large basic exemptions so

the tax system is progressive.

Hall and Rabushka argue their plan would

not only lead to a simpler tax system – tax forms for most citizens and businesses

would be half a page long, at most – but also promote efficiency and hence economic

growth in the long run. The current system, they argue, is too complex and poorly

designed, leading to unanticipated and negative consequences. For example, U.S.

employers are increasingly paying their employees in “fringe benefits” in lieu

of wages or salary because they can deduct these benefits as expenses. At the same

time, employees receive the benefits tax-free. A flat tax system would treat these

kinds of compensation equally and lead to higher pay for employees who would then have

more freedom to make decisions in their own best interest (about, for example, life

insurance) rather than have them imposed by an employer whose motivation may be purely

tax-driven. The economy, as a whole, would consequently enjoy efficiency gains.

Similarly, Hall and Rabushka argue their

one-year write-off provision would increase investment because firms would have a strong

incentive to add to their physical capital (machines, buildings, factories) because of the

tax savings. The two academics also argue that investment would increase because

their flat tax proposal is a true consumption tax. To the extent the economy is

constrained by an inadequate supply of savings, a flat tax would improve the

economy’s growth prospects by encouraging saving, which would lower interest rates

and make investment in physical capital more attractive.

By the mid-1990s, at least eight flat tax

proposals – most of them hybrids of the Hall-Rabushka proposal and the existing tax

system – were on the table in the United States. Many of these had been put

forward by Republican presidential candidates but some also came from Democratic

representatives (Banks, 1996). The bipartisan nature of these proposals speaks to

the fact that a flat tax has the potential of being fair to low-income families and

individuals provided it features some kind of large minimum deduction. Most of the

proposals followed the Hall and Rabushka plan in spirit but did not eliminate key

deductions, one of the most important being the deductibility of interest payments on home

mortgages, so cherished by Americans; the construction industry lobby had a strong

interest in retaining this feature of the tax code. The end result was that most

flat tax proposals were not revenue-neutral: absent draconian spending cuts, they

would have implied increased deficits, something that was not politically palatable in the

mid-1990s.

However, the idea of a flat tax on income

– minus the name “flat tax” – dates much further back than the

1980s. In fact, the idea of taxing all personal and business income at the same rate

is as old as the income tax itself, at least in the United States. In the late 19th century,

for example, proponents of a U.S. proportionate (i.e., flat by another name) tax saw it

mainly as a means of redressing regressive tariff and excise taxes, which at the time

accounted for the bulk of government revenue.(5)

In the context of that era, any kind of income tax, including a flat tax, was seen

as a “fair” means of attenuating the dramatic rise in inequality that

accompanied rapid technological change and industrialization in the late 19th

century.(6)

In Canada, the federal government began

taxing personal income in 1917 to pay for the large expenses incurred for the war effort.(7) Until that point, “Ministers of Finance

had contrived almost annually in their budget speeches, by the use of most inadequate

statistics, to prove to their own satisfaction that Canada was one of the lowest taxed

countries in the world” (Perry, 1955, p. 144).(8)

Although initially seen as only a temporary measure to meet pressing needs, income taxes

quickly became a fixture of government fundraising, especially with the twin crises of the

Great Depression and the Second World War, both of which helped consolidate the federal

government’s jurisdiction in this area.(9)

From the beginning, Canada’s income

tax system was progressive, perhaps due to the fact that many were concerned about war

profiteering by industrialists. Although all income was taxed at a so-called

“normal” rate of 4%, “graduated surtaxes” of 2% (on income of $6,000)

to 25% (on income of $100,000 or more) were imposed once certain income thresholds were

crossed. The tax system also included basic personal exemptions of $3,000 for

married persons and $1,500 for single persons on the normal tax rate (and not the

surtaxes), which added another heavy layer of progressivity to the tax system. One

estimate suggests that the original income tax system affected at most 1% of the total

population.(10)

The original Income War Tax Act was

a simple document, taking up all of ten pages. It was little changed until

1962, when the Carter Commission recommended a more comprehensive tax base. After a

series of public hearings and a White Paper on Tax Reform, new legislation was introduced

in 1972 that modernized the tax act, effectively repealing and replacing virtually all of

the old tax laws and forming the backbone of Canada’s current system.(11)

THE

FLAT TAX IN OTHER COUNTRIES

Despite the superficial intuitive appeal

of the idea and the high-profile nature of the U.S. debate, the flat tax has been adopted

by only a handful of countries. The most widely cited historical example is Hong

Kong, which imposes a maximum tax rate of 15%.(12)

Business groups have cited the country’s flat-tax system as an important part of the

Hong Kong economy. There are, however, many other factors that contributed to Hong

Kong’s strong growth. In fact, it seems unlikely that the flat tax alone or

even in large part explains Hong Kong’s success because other economies with much

different tax structures but similar cultural and geographic characteristics (Japan, for

example) have had similar trade records.

The so-called “transition

economies” (i.e., former Eastern Bloc countries) seem to be the most willing to

experiment with the flat tax idea. Estonia established a flat tax in 1994 and Latvia

followed suit in 1995. In August 2000, Russia adopted a 13% flat tax on income in an

effort to meet its revenue needs. Under Russia’s old tax system, which imposed

a graduated tax rate ranging from 12% to 30%, taxation revenue consistently fell short of

the government’s objective because of tax evasion coupled with the government’s

inability to enforce its tax laws. Again, it is too early to say – and, to our

knowledge, no study has shown – whether the flat tax had a positive effect on

Russia’s economic growth or government revenue.

The appeal of the flat tax to the

transition economies makes some intuitive sense given the historical record. As

discussed earlier, the idea of a flat tax first came onto the scene at about the same time

as income taxes and that is, arguably, when it had its best chance of being implemented.(13) To the extent that the transition

economies are relatively new to capitalism and are “starting from scratch,”

there are far fewer obstacles to imposing a flat tax system. Indeed, many flat-tax

proponents in the U.S. and Canada acknowledge that the biggest political obstacle to their

plan is the fact that the current tax system is entrenched both at the institutional and

personal level, where many persons either make a living off the complexity of the system

(tax lawyers and accountants, for example) or are subsidized through the tax system

(the construction industry in the United States, for example).

KEY FEATURES OF THE CURRENT TAX

SYSTEM

The “core” of Canada’s

current tax code has remained remarkably unchanged since 1988. From 1988 through to

the beginning of 2001, there were three marginal tax rates of 17%, 26% and 29%.(14) Both the tax rates and the tax thresholds

(the levels) were little changed throughout,(15)

adding an element of regressivity to an otherwise progressive tax system:

individuals whose income rose in line with inflation below 3% often found themselves in a

higher tax bracket even though their “real” situation in terms of income (i.e.,

after inflation but before taxes) had not changed.(16)

Almost by default then, the 2000 budget represents some of the most radical changes to the

income tax system since 1988.

First, it restored full indexation for

all tax thresholds as well as the basic exemption.

Second, it laid out a plan to reduce

marginal tax rates, starting with a cut in the middle rate to 25% beginning 1 July 2000.

Third, it increased the tax thresholds

at which the marginal rates apply. The lowest rate applied to the first $30,004, the

middle for the next $30,004, and the top rate to income above $60,008.

Fourth, it reduced the capital gains

inclusion rate to 66.6% from 75%.(17)

Since then, the government has introduced

further tax cuts. Beginning in January of 2001, the lowest tax rate fell to 16%, the

middle rate was cut to 22%, and income between $60,000 and $100,000 now faces a 26%

marginal tax rate instead of 29%. Income in excess of $100,000 will still be taxed

at 29%. The capital gains inclusion rate was further reduced to 50%, and the plan to

cut all corporate tax rates to 21% (service-sector and high-technology firms generally

face higher tax rates – the 2000 Budget dropped the tax rate for these firms to 27%)

was accelerated.

ARGUMENTS FOR AND AGAINST

As with most policy proposals, the flat

tax proposal(18) has its advocates and

opponents. From a political perspective, flat-tax advocates usually argue a

flat tax has three key “selling points.” They are:

Simplicity: a true flat tax

plan would eliminate frustrating and wasted hours spent trying to cope with extremely

complex laws and would, consequently, reduce and maybe even eliminate the need for tax

planners, tax consultants and tax lawyers.

Equity: The plan is at

least as, if not more, horizontally equitable than the current tax system which, for

example, sometimes discriminates against single-person households. For example, a

family with a combined income of $60,000 (assuming each spouse makes $30,000) will pay

less tax under a graduated tax system than a single person earning the same income.

Vertical equity (progressivity) can also be assured given large enough exemptions.

Revenue Neutrality: The

plan can be revenue-neutral for two reasons. First, the lower and more

straightforward tax rate means there’s likely to be less tax evasion. Second,

by design, a pure flat tax should tax a larger base, albeit at a lower rate. In

other words, a broader “swath” of income is taxed than under the current system,

compensating for the lower tax rate.

There are a number of less tangible economic

arguments in favour of a flat tax, most of which hinge on efficiency

considerations. They include:

– Payment through

“benefits” in lieu of wages/salary (discussed earlier). Again, this is

inefficient to the extent that what the corporation chooses for its employees does not

match what they would have chosen if they had been compensated with higher salaries.

– Double taxation of

savings. Dividend income under a flat tax proposal would only be taxed

once. Similarly, capital gains income would be taxed only once at the corporate

levels and no longer at the personal level.(19)

Thus, corporations would make their financing decisions (i.e., to borrow, sell shares or

float bonds) independent of the tax structure.

– Labour market

distortions. Under the graduated tax system, some employees may be reluctant to

take a higher-paying job if it means paying more taxes. To the extent that this

happens, the current system reduces efficiency: society as a whole would benefit

from that person working to his/her potential.

More accurate prices: The

flat tax would mean that tax considerations would no longer have such a distortionary

impact on prices. Decisions would be made for purely economic reasons or on the

basis of individual preferences, relatively unimpeded by tax considerations. Prices

should therefore more accurately reflect true supply and demand conditions.

Increased savings and investment:

By taxing income only once, a flat tax should lead to increased savings which, in turn,

theory suggests could lead to lower interest rates and more investment. The one-year

write-off provision also holds out the promise of more investment.

Faster growth and higher

productivity: All things being equal, a flat tax would lead to more investment

which should improve productivity and lead to stronger economic growth. This in turn

could have feedback effects on the federal government’s budgetary position.

Increased transparency: A

flat tax would mean that all tax increases (and decreases) would be extremely visible and

clear, unlike under the current system. For proponents of the flat tax who

favour smaller government, this could be a strong selling point because all

tax increases to finance more government spending would probably entail a large

“political cost.”

There are, of course, a number of

arguments against a flat tax. Flat tax opponents usually make two

“visible” or popular arguments against the tax:

A flat tax violates the common notion

of fairness which differs from economists’ vision of the concept.(20) Although it’s true that a flat tax

can be progressive, it is also true that moving to a flat tax means that higher-income

families receive the bulk of the benefit of a given tax cut in absolute terms. As

noted earlier, this is to some extent inevitable because even a small percentage reduction

in tax rates for very high-income families translates into a large absolute tax

saving. Nevertheless, giving “more” in absolute terms to the wealthy seems

to violate popular notions of fairness. The popular sense of fairness also seems to

be transgressed by the image of a wealthy person living off of his/her savings (either

through capital gains or dividend/interest payments) without personally paying any

income tax,(21) especially if he/she inherited

the money or earned it through luck rather than hard work.

Flat-tax proponents exaggerate the

benefits of their proposal.

– Most people already

have very simple tax returns. In the United States, for example, citizens can

file simplified tax forms that are only a page long. The benefit of

“simplifying” the tax code, therefore, really only accrues to the

well-off.

– Flat tax plans are

unlikely to be revenue-neutral because by design they aim to reduce the top marginal

rate while providing large basic exemptions for low-income earners. This

“you-can’t-have-your-cake-and-eat-it-too” argument says that a larger tax

base won’t be enough to make up for the lost revenue and nor will the promised

economic growth, improved efficiency and greater tax compliance. Assuming this

non-neutrality then, a flat tax would likely mean reduced spending on social programs,

including those targeted to low-income persons. Thus, although low-income persons

may pay less in taxes (and, indeed, receive larger tax rebates), they may lose at least as

much from reduced transfer payments.

There are also a number of economic

arguments against the flat tax:

A flat tax may attenuate the

counter-cyclical effects of the current system. For example, during an

expansion, government revenue tends to rise quickly under a formally progressive tax

system, essentially “dampening” some of the excesses of the cycle. The

reverse occurs during a downturn. Although no one is sure of the dynamics of a flat

tax under a business cycle, it seems at least plausible to suggest that the dampening

effects wouldn’t be as great. For example, investment tends to move

pro-cyclically, i.e., it increases as the economy nears its peak and falls as it hits a

trough. All things being equal, the one-time depreciation part of the Hall and

Rabushka flat tax proposal would effectively reduce government revenue (relative to the

existing system) at the peak and increase it in the trough, accentuating the cyclical

highs and lows. This could imply more acute economic ups and downs.

Although popular notions of fairness

may not accord with economists’ vision of the concept, they should not be dismissed

out of hand. As former Canadian Economics Association President Lars Osberg

suggested in an article on trends towards worsening inequality in Canada,(22) civil society (volunteerism, the willingness to pay taxes,

abide by laws, help out) is perhaps more fragile than commonly thought. As Russia

and other lesser-developed countries show, there is a very real danger that the fabric of

civil society can be destroyed when policy-makers impose abrupt changes to the

institutional structure, of which the tax system is an important part. Also, a flat

tax inevitably implies a greater tax cut in absolute terms for high-income

individuals/families and the wealthy; this could mean a worsening of inequality,

especially if the flat tax is not revenue-neutral and social programs are consequently

cut. Even if the tax is revenue-neutral, a flat tax could mean worsening inequality

in the long run if only because high-income earners and the wealthy are generally better

able to invest their tax savings and make them grow more quickly than are low-income

persons.

A flat tax has ambiguous labour

market effects. Although most economists agree that a flat tax would have a

positive substitution effect (i.e., people would want to work more knowing their income

would be taxed at a lower rate), the income effect is less clear: because they get

to keep a greater share of their income, some workers may choose to work less because they

can still achieve the same level of consumption as before the tax cut. There is no a

priori way of knowing which effect will dominate or even if these two effects are the

relevant ones; sociological factors may dominate. Some arguments in favour of a flat

tax are open about this ambiguity. For example, the case is frequently made that the

current system discriminates against single-income two-parent households, suggesting that

there is an incentive for both partners to work at lower wages than would be the case

under a fairer system. Doing away with these incentives via a flat tax could,

perversely, reduce labour force participation.(23)

The lack of taxation on capital gains

could worsen income inequality (and violate the popular perception of fairness) to the

extent that the market does not, in fact, perfectly “price-in” future

earnings. Put another way, if markets are prone to herd-like behaviour, as the

recent collapse of the “dot.com” craze suggests and as some research into the

psychology of investors indicates, then some investors may sometimes earn large capital

gains with no “real” underpinning, that is, they obtain money for nothing

(often, companies whose shares soar end up going broke – the Canadian mining firm of

Bre-X being a classic example). This is a perverse form of income redistribution not

based on work effort but on gambling skills and luck.(24)

It could be argued that Canada

already has a flat tax of sorts – for those whose income exceeds the top

threshold (soon to be $100,000 but currently $60,008). This should, all things being

equal, provide sufficient incentive to draw workers into the labour force. In other

words, a formally progressive system with a flat tax at the top may perversely incite

people to work harder, especially if their utility is augmented by the higher social

standing that usually goes with more income.

THE BUDGETARY CONSEQUENCES OF A

FLAT TAX

Up to now, the discussion in this paper

has been rather abstract. This section attempts to present a real-world sense of the

budgetary consequences of a flat tax that retains most of the current system of deductions

and tax credits. It is important to stress this is very much unlike the Hall and

Rabushka proposal that has been examined throughout most of this paper. The

rationale for looking at this hybrid flat tax is simply that significant institutional

changes are rarely implemented except in times of crisis. This task begins with a

question: What is the lowest flat tax that could be imposed if all the features (tax

cuts and spending initiatives) implemented in the most recent budget documents (Budget

2000 and the economic supplement) were retained and an assumption was made that future

governments are committed to: a) maintaining at least a balanced budget; b)

increasing nominal expenditure at the same rate as population growth plus inflation; and

c) reducing the debt by at least $6 billion per year? This is clearly a difficult

question given the complexity of the tax code. Fortunately, Statistics Canada has

developed a model called the Social Policy Simulation Database (SPSD/M) that gives a sense

of what a flat tax policy would cost given these conditions. Before looking at the

results of this experiment, two important cautionary remarks are in order:

First, as with all models of this kind,

one should heavily discount projections beyond a year or two for the simple reason that

the assumptions girding the model are very quickly made obsolete by real-life

events. The safest projections are the ones nearest in time.

Second, the SPSD/M model is

“static” in that it does not allow for any kind of economic growth. All

projected revenue increases arise out of nominal (inflationary) changes in measured

output. This is important because flat tax proponents generally argue that their

measures would stimulate economic growth through improved efficiency and possibly

increased spending.(25)

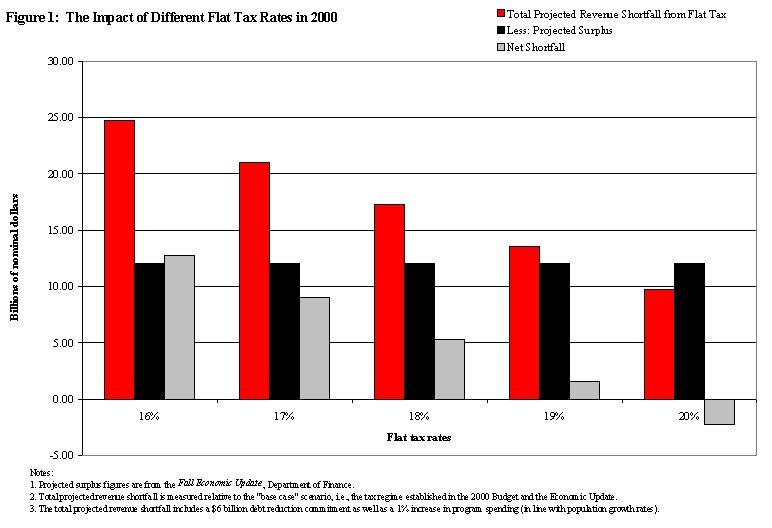

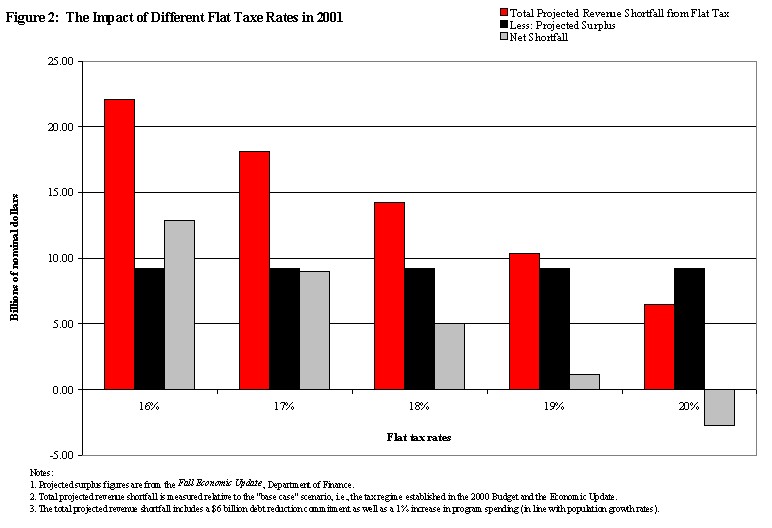

Figures 1 and 2 show results for the

calendar years 2000 and 2001.(26) The

charts show clearly that a revenue-neutral flat tax – given the proposed spending

increases, debt reduction plans, and existing system of deductions and credits –

would have to be somewhere between 19% and 20%. Again, it must be stressed that the

figures in this paper were calculated relative to the base case, namely the tax system

modified for changes in the 2000 budget as well as the fall economic statement. Note

also that the total cost figures include the effects of putting in place a flat tax plus

1% annual spending increases (in line with population growth) and $6 billion in

annual debt reduction debt.

CONCLUSION

The discussion in this paper has attempted

to provide a relatively complete contextual picture of the flat tax by looking at its

historical roots, its modern-day uses, and arguments for and against the idea. Some

likely budgetary consequences of the tax, given the structure of a politically plausible

proposal and the current tax system, have also been considered. These calculations

should be viewed as merely suggestive. Much can happen in a year or two that would

invalidate these figures, potentially making this kind of flat tax more or less

feasible. If one conclusion were drawn from this analysis, it might be this:

the historical and international record suggest that the odds of moving towards a flat tax

increase greatly after an abrupt and dramatic failure of the existing tax system (Russia)

or at the earliest stages of an income tax system (Estonia, Latvia and Hong Kong).

Short of that, the sheer inertia behind the existing tax system invariably corrupts flat

tax proposals beyond recognition, weakening or destroying most of the idea’s

strongest selling points and ultimately cutting into the revenue-generating potential of

the proposal. This in turn threatens core programs, and that may entail high

political costs.

REFERENCES

Alliance Party. 2000.

“Solution 17.” Internet: http://www.canadianalliance.ca/index_e.cfm.

Beauchesne, Eric. 13 September

2000. “Canada Duplicating U.S. Economic Miracle.” The Ottawa

Citizen, Internet edition: http://www.ottawacitizen.com/.

Canada. 1987. “The White

Paper on Tax Reform: 1987.”

Canada. Department of Finance.

2000. “The Budget Plan 2000.” Department of Finance Distribution

Centre.

Chernick, Howard and Andrew

Reschovsky. September-October 2000. “Yes! Consumption Taxes are

Regressive.” Challenge Magazine, pp. 60-91.

Gillespie, Irwin W. 1991. “Tax,

Borrow & Spend: Financing Federal Spending in Canada: 1867-1990.”

Ottawa: Carleton University Press Inc.

Hall, Robert E. and Alvin Rabushka.

1995. The Flat Tax. Stanford, California: Hoover Institution

Press.

Lerner, S., C.M.A. Clark and W.R.

Needham. 1999. “Basic Income: Economic Security for All

Canadians.” Toronto: Between the Lines.

Moore, Stephen. 14 January

1997. “The Alternative Maximum Tax.” Editorial, Wall Street

Journal.

Perry, David P. 1997.

“Financing the Canadian Federation, 1867-1995: Setting the Stage for

Change.” Toronto: Canadian Tax Foundation.

Perry, J. Harvey. 1955.

“Taxes, Tariffs and Subsidies.” Toronto: University of Toronto

Press.

Rosser, J. Barkley Jr. and Marina

Vcherashnaya Rosser. 2001. “Inequality and Underground

Economies.” Challenge Magazine, pp. 39-50.

Slemrod, Joel. 1996.

“Deconstructing the Income Tax.” American Economic Association

Papers and Proceedings, pp. 151-155.

Vickrey, William. 1987.

“Progressive and Regressive Taxation.” In Eatwell, John, Murray

Milgate and Peter Newman, eds. The New Palgrave: A Dictionary of

Economics. London: MacMillan Press.

(1) Flat

tax proposals have also been made by Member of Parliament Dennis Mills. As well, the

Progressive Conservative Party briefly considered the idea of a flat tax, as did the

Reform Party, the predecessor of the Canadian Alliance.

(2) It

is, of course, possible to imagine that the no-children family is burdened with large

medical costs for one or both spouses or is looking after ill grandparents.

(3) See,

for example, Nobel Prize winner William Vickrey’s definition of progressive and

regressive taxation in the New Palgrave dictionary. What he calls “formally

progressive” refers to the idea of different marginal tax rates applying to different

income classes. However, he notes that even taxes and tax systems normally

considered regressive can be “modified to reduce the degree of regressiveness or even

render them moderately progressive.” An alternative way of achieving a progressive

flat tax structure would be to tax all income (no exemptions) equally but combine that

system with a large tax credit, essentially putting in place a negative tax or basic

guaranteed income provision. See S. Lerner, C.M.A Clark and W.R. Needham’s

“Basic Income: Economic Security for All Canadians” for one such

proposal. Alternatively, a tax system with adequate exemptions and/or deductions

– such as the Robert Hall and Alain Rabushka flat tax proposal and some of its

variants – could achieve a similar blend of horizontal and vertical equity.

(4) This

assumes that all else is equal, i.e., that the flat tax doesn’t somehow lead to cuts

in social welfare programs that transfer money directly to lower-income families.

(5) This

was true in Canada as well; see Perry (1997). Tariff and excise taxes were, and to

the extent that they still exist are, regressive when they apply to goods and services

that take up a greater share of the revenue of a low-income family or individual than of a

wealthy family or individual because manufacturers are generally able to pass along the

taxes in the form of higher prices. For example, excise taxes on gasoline are

generally thought to be regressive because there is evidence that low-income families and

individuals spend more of their total income on gasoline than do high-income families or

individuals. However, as Gillespie (1991) shows, Canadian officials were

historically reluctant to impose excise taxes on basic goods (coffee, tea, food) because

of concerns about attracting and keeping immigrants who tended to spend significant

portions of their income on these items. Most taxes were applied to so-called

“sin” items such as alcohol. This was made politically feasible because

of the forces promoting prohibition.

(6) The

first, general income tax was enacted in Great Britain in 1799, to finance the Napoleonic

War. The tax was subsequently repealed and re-introduced in the 1880s, when it was

generally accepted as a permanent fixture of government finance.

(7) Income

taxes were levied by some provinces before World War I.

(8) Perry

argues there is reason to doubt those who claimed that pre-war Canada was a “tax

haven,” citing work by Dr. O.D. Skelton showing Canada’s average per capita tax

was $31.50, compared with $24.63 in England and $30.90 in the United States (p. 145).

(9) See

David B. Perry’s “Financing the Canadian Federation, 1867-1995: Setting

the Stage for Change,” Toronto: Canadian Tax Foundation, 1997.

(10) This

historical overview is from Gillespie (1991).

(11) The

CCH Canadian Ltd. summary of the income tax act – including all technical notes,

pending amendments, Department of Finance Press Releases, and notices of ways and means

– weighs in at about 1,890 pages.

(12) Hong

Kong residents can choose between paying the flat 15% rate on income or the more

traditional tax system, with its attendant deductions and exemptions. Some have

proposed this kind of model, called a MAXTAX, for the United States. See Moore

(1997) for a discussion of the MAXTAX proposal.

(13) The

idea of a flat tax is intricately bound to that of the income tax, even when it exists in

opposition to an income tax system (i.e., consumption taxes).

(14) Prior

to 1988, there were ten marginal tax rates, ranging from 6% on the first $1,320 to 34% on

taxable income exceeding $63,347.

(15) The

tax thresholds in 1988 were $27,500 and $55,000 versus $29,590 and $59,180 at the

beginning of 2000. That represents a 7.6% increase during a 12-year period compared

with a 30% increase in the consumer price index over the same period.

(16) Although

tax thresholds (brackets) were indexed to inflation above 3%, this meant little in

practical terms because the Bank of Canada pursued an aggressive policy of keeping

inflation below this threshold. It was successful for most of the decade.

(17) These

were the short-term effects of the tax plan. The medium-term plan was to reduce the

middle-income tax rate to 23% and increase tax thresholds to $35,000 for the lowest

marginal rate and $35,000 to $70,000 for the middle rate. These higher thresholds

are the result of both a basic “bump up” in the threshold plus full

indexation. Indexation also was projected to increase the basic personal exemption

to $8,000 from $7,131 within five years. The plan also increased the Canada Child

Tax Credit to $2,400 by 2004 and eliminated the 5% surtax for persons with incomes up to

$85,000.

(18) The

reference to “flat tax” here means the Hall and Rabushka proposal which appears

to be the most thoroughgoing and most discussed of existing proposals.

(19) The

rationale is similar to that of taxing dividends only once. Consider, for example,

company shares, which in theory represent the capitalized current value of after-tax

future earnings. A capital gain is recorded when the price of these shares rise

based on expectations of increased future profits. These future profits will be

taxed when, and if (markets are not, after all, omniscient), they occur. Because the

goal is to tax all income only once, it makes no sense to tax them in the hands of the

shareholder who realizes this capital gain.

(20) Recent

research in the burgeoning field of economics and psychology suggests that common notions

of fairness are severely at odds with the economist’s vision of fairness.

(21) This

income is, however, taxed at the source (i.e., at the corporate level).

(22) Lars

Osberg, “Poverty in Canada and the USA: Measurement, Trends and

Implications,” Presidential address to the Canadian Economics Association, Vancouver,

3 June 2000. Available online at

http://is.dal.ca/~osberg/uploads/Povtrend.PDF.

(23) This

is seen as a selling point by some flat tax advocates who want to encourage stay-at-home

mothers or fathers.

(24) Inequality

may have direct economic impacts as well. For example, J. Barkley Rosser and Marina

Vcherashnaya Rosser (2001) present empirical evidence that suggests heightened inequality

may encourage the growth of black markets that erode the government’s revenue base.

(25) Some

economists argue the principle that benefits would come from efficiency gains because the

tax effects are nil in the long term.

(26) Note

that these are calendar year figures while budgetary projections are generally done in

fiscal years ending 31 March. To compensate for this discrepancy, the paper’s

analysis has assumed that one-quarter of the surplus for 1999-2000 and three-quarters of

the projected surplus for 2000-2001 represented the equivalent “calendar year”

surplus for 2000. This yielded a projected surplus of $12 billion for calendar

year 2000 instead of $11.9 billion for 2000-2001 and $9.2 billion for calendar year

2001 instead of $8.3 billion for 2001-2002.