Parliamentary Research Branch

PRB 98-2E

THE RELATIVE POSITION OF CANADA

IN THE WORLD GRAIN MARKET

Prepared by:

Sonya Dakers, Science and Technology Division

Jean-Denis Fréchette, Economics Division

September 1998

Averaged over a ten-year period (1986 to 1995), Canada occupies sixth place among the world’s major wheat-producing countries, preceded (in order of importance) by China, the European Union, the United States, India and the Russian Federation.

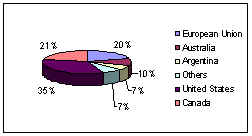

In terms of international trade, however, Canada is the world’s second largest exporter of wheat; with annual exports averaging some 20 million tonnes, this country accounts for about 21% of the world market for wheat exports.(1)

Again, averaged over a ten-year period, we find that China and Japan are by far Canada’s principal customers for wheat and flour. They are followed by Iran, South Korea, the United States, Brazil and Algeria. A new trend has been emerging, however, since the early 1990s, as the United States has moved into second place as a customer for Canada’s wheat, with average imports of Canadian wheat fluctuating around 1.5 million tonnes per year. (see Canada-U.S. Grain Trade Relations)

The excellent quality of Canadian hard wheat (durum), the type of wheat used primarily in the making of pastas and semolina, is often noted. Canada is by far the major exporter of this type of wheat, and its average annual exports amount to nearly three million tonnes, or 48% of total world exports. Algeria and Italy have traditionally been Canada’s two largest customers in this area, but demand from the United States has been growing steadily since the early 1990s.

With respect to coarse grains — barley, rye, oats, corn, sorghum and millet world production amounts to some 800 million tonnes per year. Canada produced on average 23.2 million tonnes of these grains each year over the period 1986 to 1995, including 12.5 million tonnes of barley. In recent years, Canadian output of coarse grains has tended to be above the long-term average, in particular because barley growing has been stimulated by higher livestock prices.

Corn is the most important coarse grain traded on the world market, with an average annual volume of 60 million tonnes. It is followed by barley, with a volume of about 17 million tonnes per year. With exports of only 300,000 tonnes, principally from Ontario, Canada is not a major player in the corn export market. On the other hand, its annual exports of barley have averaged 3.8 million tonnes over the last ten years, allowing it to capture 22% of world trade in brewing and feed barley to become the world’s second largest barley exporter, after the European Union. Asia is by far the most important market for Canadian barley.

While canola exports represent only 10% of world trade in oilseeds, Canada has the lion’s share of the market: its exports of more than three million tonnes a year account for 80% of total exports of canola, which amount to nearly four million tonnes per year. By comparison, Canada’s closest competitor, the European Union, exports just over 300,000 tonnes of canola a year. The main sources of demand for Canadian canola are Japan, Mexico and the United States. On the domestic market, demand for canola is growing, thanks to the development of the oil crushing industry and the making of oilseed cake. Agriculture and Agri-Food Canada estimates that the capacity of the domestic canola crushing industry could soon exceed 12,000 tonnes a day. It is hardly surprising, then, that the area devoted to canola growing in the West has risen from two million to more than five million hectares over the last 15 years, primarily in Saskatchewan and Alberta.(2) While output and export levels are still far below those for wheat, there is a steady upward trend in the canola market, and the numerous private investments in the processing sector confirm that expectations are high.

World Wheat Export Market Shares

(May 1986-1995)

Major Export Markets for Canadian

Wheat

(Including Durum)

(in thousands of tonnes)

Average |

|

China |

4,448 |

(1) The statistics cited in this section are taken from annual reports of the Canadian Wheat Board and from statistical compilations of the Canadian Grain Commission and Statistics Canada, Cat. 22-201.

(2) Source: Agriculture and Agri-Food Canada, Policy Branch, Market Analysis Division.